According to the Reserve Bank of Zimbabwe (RBZ) and the government, the ZiG is the official, legal, gold-backed currency of this country. You are supposed to trust it, save in it, pay with it, and believe in it. The state has done everything it can to make that case on paper.

In the February 2026 monetary policy statement, RBZ governor John Mushayavanhu raised ZIPIT and mobile money transaction limits from ZiG 8,000 to ZiG 13 000 per transaction, with a monthly cap pushed to ZiG 50,000 all to promote wider ZiG usage, so he said.

The RBZ also introduced new, larger denomination ZiG banknotes 10, 20, 50, 100, and 200 ZiG notes to improve cash handling across the economy. Government suppliers are required to accept it. The policy machinery is fully behind it.

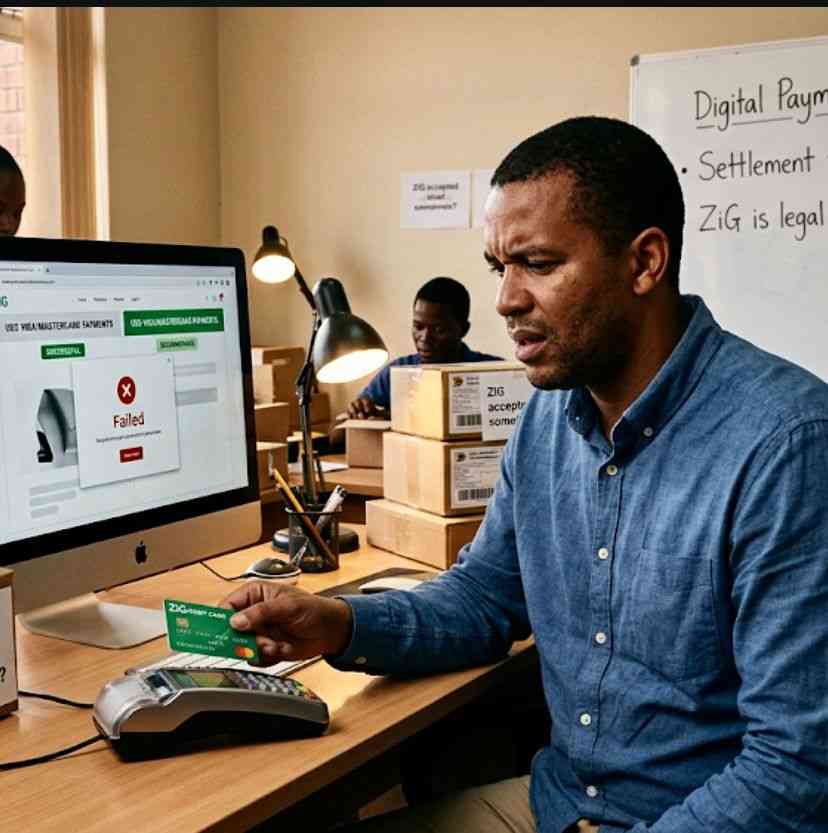

But yet there is a digital glitch in the matrix. If you try to book a ride-hailing app, or pay for groceries on a local website, your ZiG card often feels like a plastic coaster.

Meanwhile, USD Visa and Mastercards breeze through the checkout.

If the ZiG is legal tender, why is our own digital economy treating it like a second-class citizen?

The payment gateway problem nobody talks about

The backbone of online payments in Zimbabwe runs through a handful of platforms Paynow, Pesapal, DPO Group, and a few others.

- Awards target married couples

- Awards target married couples

- Rampaging inflation hits Old Mutual . . . giant slips to $9 billion loss after tax

- Monetary measures spur exchange rate stability: RBZ

Keep Reading

These gateways are what connect a merchant's website to your bank account. Paynow, widely considered the leading payment gateway in Zimbabwe, does support multiple payment types including Visa, Mastercard, EcoCash, and Zimswitch.

On paper, ZiG card payments should flow through Zimswitch.

In practice, the experience for many users is far bumpier than that for USD card holders.

Part of the problem is on the merchant side. Most local e-commerce operators do not configure ZiG card acceptance as a default they set up USD card flows because that is where their revenue certainty lies.

Merchants who are paid in ZiG also face a settlement delay.

Paynow settles local Visa and Mastercard transactions two days after the payment date, and foreign Visa and Mastercard payments three days after.

There is no publicly available breakdown of how ZiG card settlements compare, or whether the T+2 settlement applies equally regardless of currency.

That opacity creates merchant risk and where there is uncertainty, merchants quietly default to USD.

The consumer experience is equally messy. Many ZiG-denominated cards issued by local banks are not automatically enabled for online transactions.

Customers often have to request online activation separately and even then, some cards get routed to bank USSD prompts mid-checkout, which is jarring and unreliable on a website.

Meanwhile, a person using a USD Visa card sails straight through.

The fees that nobody is enforcing consistently

The RBZ has tried to fix some of this. From April 1, 2026, POS charges are capped at 1.5% of the transaction value for both local and international cards, with no minimum fee allowed and a maximum cap of US$20 or the ZiG equivalent.

That is a welcome directive. But a directive is not implementation.

The RBZ's own governor acknowledged in the same policy statement that the central bank continues to receive complaints from the public about the high cost of banking, and that excessive charges discourage people from using formal banking channels.

So even with the cap in place, the question stands: are banks applying the 1.5% rule consistently across ZiG and USD card transactions?

Or are some institutions still charging differently depending on the currency?

Nobody has published a clear answer. The RBZ needs to audit this openly, not just direct and hope.

The tax layer that makes everything worse

Then there is the 15% digital services withholding tax introduced on January 1, 2026 which applies to payments made to offshore digital service providers.

Finance minister Mthuli Ncube framed it as a way to level the playing field between foreign platforms and local businesses.

The tax is intended to apply to services like streaming, ride-hailing, and satellite internet, and is collected automatically by local banks and mobile money operators.

The distinction matters, ZiG card transactions at local merchants should be exempt from this tax. It is a domestic payment, not an offshore one.

But the question nobody has publicly answered is whether banks have correctly implemented this distinction in their systems or whether all card transactions are being swept into the same withholding bucket.

The intermediated money transfer tax already applies a 2% charge on USD transfers and 1.5% on ZiG transactions, meaning combined tax loads can pile up quickly.

If the 15% DSWT is also being incorrectly applied to local ZiG card transactions, customers are being overtaxed in silence.

The trust deficit behind all of this

The honest truth is that none of this is purely a technical problem. It is a trust problem, and the infrastructure reflects it.

At the time ZiG launched in April 2024, US dollars already accounted for four-fifths of all transactions in Zimbabwe. ZiG was introduced to correct that but by October 2024, just six months after launch, ZiG had officially lost half its value on the regulated market and suffered a 75% loss on the unregulated one.

Merchants who had priced goods in ZiG and accepted ZiG payments found themselves holding a currency worth far less than when the sale was made.

Of course they migrated back to USD.

Of course, payment gateways optimised for the dollar flow. Of course, local e-commerce platforms built their checkout UX around the currency that holds value.

Zimbabweans have developed a deeply entrenched culture of cash-based transactions in stable foreign currencies, rooted in a justifiable fear that bank balances held in local currency will be abruptly converted or devalued because that has happened before.

The online payment infrastructure is simply a mirror of that fear.

What needs to happen

This is not an argument against ZiG. It is an argument for honesty about where ZiG actually sits in the digital payment stack and for fixing the gap between the government's rhetoric and the consumer's lived experience.

The RBZ Payments Division needs to put on record exactly which banks currently issue ZiG-enabled online cards, what the activation process is, and what the settlement timelines are for ZiG card transactions at local merchants.

Paynow and other gateways need to state publicly whether ZiG card support is configured by default or by merchant request, and what the technical failure rate looks like compared to USD transactions.

Local e-commerce operators need to be willing to share concrete examples of how many ZiG card checkout attempts fail versus succeed not in aggregate digital payment numbers, but specifically in online card flow.

Zimbabwe's digital payments reached a record US$5.93 billion in retail transactions in Q2 2025, a 34% increase from the previous quarter so the digital infrastructure is growing. The volume is there.

The rails exist.

What is missing is the political honesty to admit that ZiG has not yet earned the same trust as the USD in digital commerce, and that trust cannot be legislated into existence through transaction limit increases and policy statements.

You can raise ZIPIT limits. You can print bigger notes. You can mandate ZiG acceptance for government suppliers.

But if a Zimbabwean woman in Harare tries to buy a dress from a local online boutique using her ZiG card and gets an error screen while her colleague breezes through the same checkout with a USD card then ZiG is not yet king of anything that matters in the digital economy.

Fix the checkout. Then we can talk about the currency.